| Victor V. Zhorin

|

| Research areas: scientific computings, financial systems and growth, deep uncertainty quantification, big (complex) data analysis |

Research Projects

New PapersThe Mortality Input Problem:

Trajectory-Dependent Death and the Lifecycle Model The first lifecycle model in which death is endogenous Mortality Prediction as Boundary Value Problem, The framework unifies perspectives from causal set theory, rough path theory, tropical geometry, and viscosity solutions with respect to predicting mortality Why Financial Event Sequences Require Temporal Transformers:

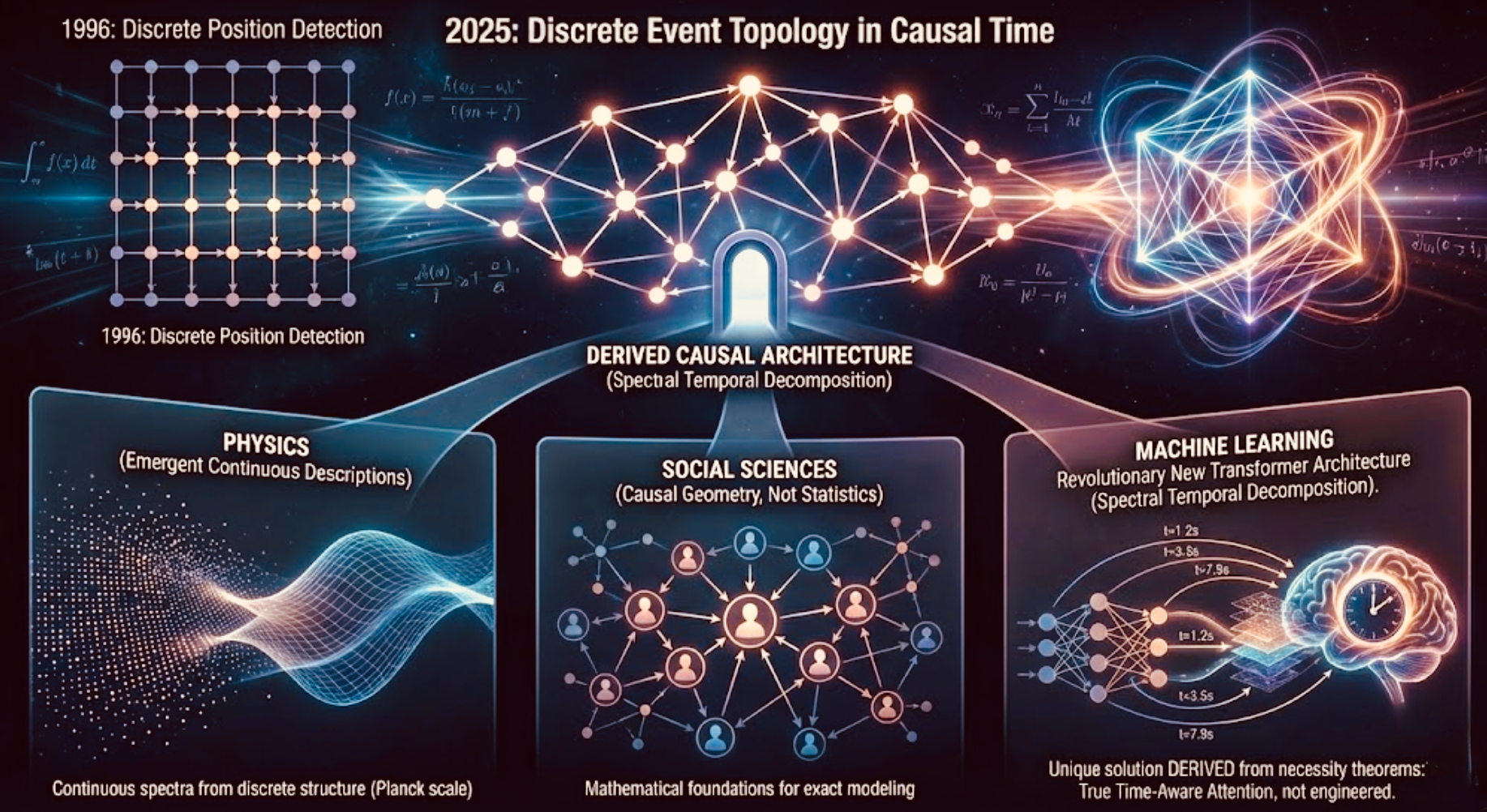

Necessity Theorems for Default Prediction, The theoretical framework identifies minimal requirements for financial sequence modeling and explains observed performance gaps between sequential and tabular approaches in credit scoring. Causal Set Topology for Transformer Architectures: From Planck Scale to Human Life,

Mathematical unification connecting causal set theory in quantum gravity to temporal modeling of human trajectories. The same tensor operations describing discrete spacetime describe a patient evolving through clinical events. |

Socioeconomic modeling Climate-economic linkages, detection of economic growth patterns using sattelite data, VVUQ for economic models with financial sectors |

Robust Decision Making Numerical analysis of robust stochastic macroeconomic models in continuous time with optimal control and financial sector |

Work in progress: tensor-based computing